Property Market

Property Market

11 May 2026

68 Days to Sell a Chelmsford Home… Unless You Get This Wrong

If you are a homeowner or landlord in Chelmsford and th…

Property Market

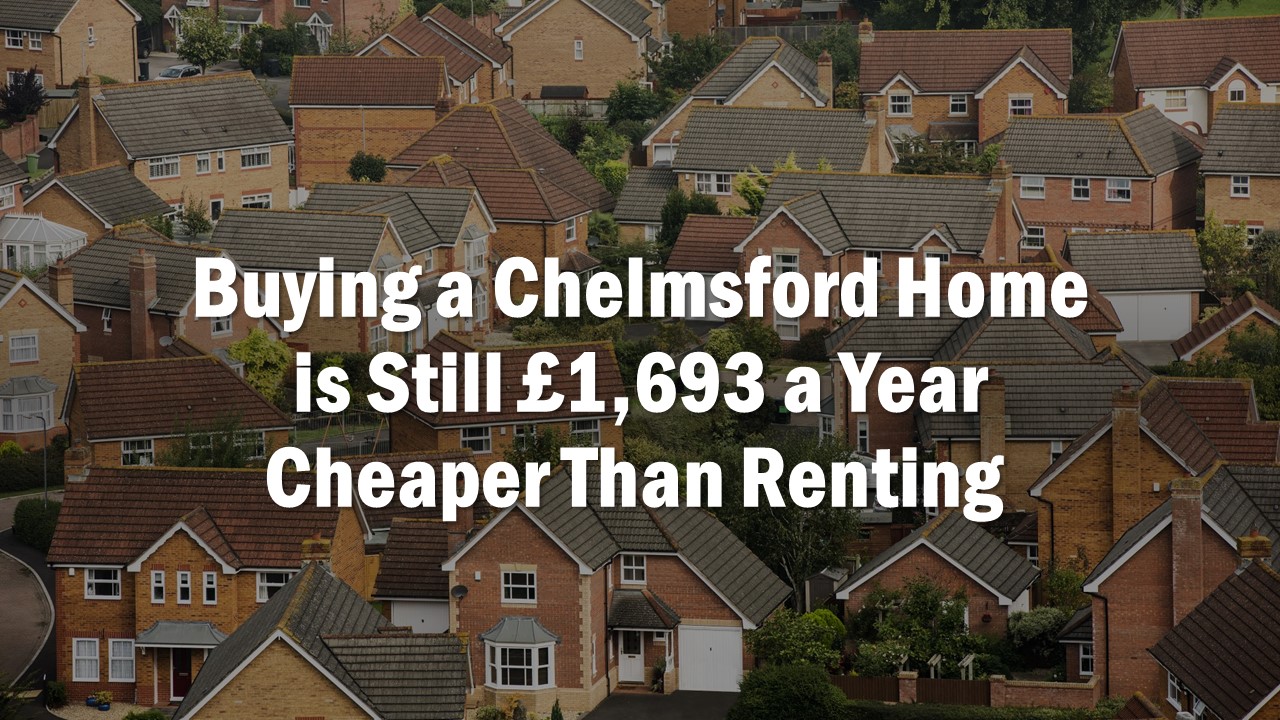

With mortgage rates tripling over the last 12 months, one could be forgiven for thinking buying a Chelmsford home as a first-time buyer would out of the question.

Yet, what if I told you, it is £1,693 a year cheaper to buy a Chelmsford home as a first-time buyer than renting, would you be surprised?

The monthly homeownership cost of such a Chelmsford home (including the mortgage payments, property maintenance, and insurance bills) comes to £1,178.91 per month compared to £1,320 per month for the same Chelmsford house for rent.

Because Chelmsford rents have risen like a rocket ship in the last two years, this has helped to tip the balance in favour of homeowners.

This is based on the average first-time buyer mortgage with a deposit of 23% (that being the average last year for a first-time buyer nationally) and industry recognised amounts on property maintenance, and insurance bills.

Yet I thought 23% seems quite high, so I thought what it would cost with a smaller deposit of 10%.

Before I answer that, I believe the ‘buy versus rent argument’ is more than a simple pound notes question. Let me expand.

Firstly, renting allows for short-term living arrangements, with tenancies often lasting just six months. This provides flexibility for those who want to try out a new location or property. Additionally, renters are not responsible for maintenance costs, including broken boilers, and may have the option to rent a furnished property. There are also lower upfront costs, as renters do not need to pay legal fees, maintenance costs, stamp duty or a mortgage.

Chelmsford tenants face large upfront costs, including a deposit and first month’s rent – and landlords may increase rent. Renters also lack control over maintenance and may have to move if the landlord decides to sell the property.

Additionally, they may have to battle landlords to receive their full deposit back.

On the other hand, owning a Chelmsford home provides long-term security and the ability to decorate and control maintenance. Even though mortgage interest rates have more than tripled in the last 18 months, mortgages are currently still comparatively low compared to the long-term average. Let’s not forget …

However, saving for a deposit can be difficult and homeowners are subject to the housing market and price fluctuations. They must also pay mortgage and legal fees and must foot the bill for repairs.

Let’s be frank, both renting and buying a Chelmsford home have advantages and disadvantages.

It is important for individuals to carefully consider their financial situation and personal preferences before deciding.

So, let me look at Chelmsford first-time buyers who have a 10% deposit.

Yet when that annual figure is broken down into a monthly figure, surely paying £63.84 a month, with all the advantages mentioned above, is still worth it to buy your own Chelmsford home?

To conclude, whether it’s worth buying a home or renting a home in Chelmsford depends on your personal circumstances and priorities.

While owning a home can offer security and stability, it’s important to consider factors such as your future, financial situation and long-term goals.

Before deciding, take the time to ask yourself the right questions and weigh up the pros and cons carefully. By doing so, you can ensure that you make a choice that is best for you and your family’s future.

These are my thoughts, what are your thoughts people of Chelmsford.

Lets get started! Our valuations are based on our extensive knowledge of the whole of the market.

Get a valuation

Property Market

11 May 2026

If you are a homeowner or landlord in Chelmsford and th…

Property Market

Property Market

Property Market

Property Market