Property Market

Property Market

23 Jul 2026

Chelmsford Property Market: How Q2 2026 Compared with the UK

As an agent in the Chelmsford property market, I believ…

Property Market

Since Christmas, Chelmsford first-time buyers and savvy Chelmsford buy-to-let landlords have been more active than expected in the Chelmsford property market.

Rents in the Chelmsford area have soared in the last two years, with the average Chelmsford rent increasing to £1,273 a month, an increase of 17.11%.

Because of these growing Chelmsford rents, it has made homeownership more cost-effective for younger Chelmsford buyers and more lucrative for Chelmsford landlords.

On the back of this, house prices are rising in Chelmsford.

But how can I say house prices are rising when the Land Registry and other indices from the banks state they are falling?

The Land Registry figures published this month will be from sales completed (i.e., keys and monies handed over in February 2023). Yet, as everyone knows, it takes on average, 19 weeks from agreeing on a sale to a completed sale in the UK, so those Land Registry house price figures are from house sales agreed upon in September or October 2022.

If only there were a more up-to-date way of calculating what is happening to house prices.

Well, there is!

By measuring what houses sell for at the sale agreed date by their square footage.

As I explained last week, the measure of £/sq. ft is not a particular great way to judge the value of an individual property. However, when looking at a national and regional level, its accuracy is excellent (98% accurate on a national level and around 95% accurate on a regional level).

The average price per square foot at sale agreed matches the Land Registry and Nationwide House Price Index to a very high tolerance/accuracy level, albeit 7 or 8 months before the Land Registry/Nationwide publish their data.

So by tracking the regional £/sq. ft figures for the East of England, it will give us an excellent idea of what is happening to Chelmsford house prices now.

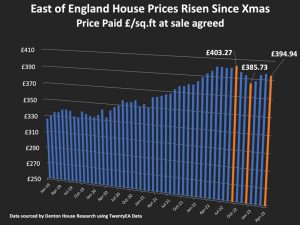

The top of the property market was in September 2022 when the average £/sq. ft achieved for all house sales agreed in the East of England was £403.27/sq. ft.

By December 2022, this had dropped to £385.73/sq. ft, a drop of 4.55% (for the East of England homes sold stc in December ’22).

By this April, the average £/sq. ft achieved for all house sales agreed in the East of England had risen by 2.33% to £394.94/sq. ft.

Let’s put it another way.

House prices in the East of England area (including Chelmsford) are 2.33% higher than at Christmas.

Just for interest, these are the £/sq. ft figures split down by property type:

Before I move on to what the future holds, as a good comparison, currently Chelmsford houses are selling for an average of £443/sq. ft.

There are several issues which could upset the ‘apple cart’.

One is the recent Bank of England base rate rise.

The recent decision by the Bank of England (BoE) to raise the Base Rate by 0.25% has only led to a negligible increase of 0.04% in average rates for two-year and five-year mortgages.

This rise in BoE interest rates is primarily attributed to their forecast that inflation will not decrease as quickly as initially anticipated.

Consequently, the underlying costs of lenders’ fixed-rate deals, known as swap rates, have risen slightly, resulting in an adjustment of lenders’ mortgage rates, but not that much.

To provide some perspective, current average mortgage rates (late May) are like those observed at the beginning of April, with some rate fluctuations in those seven weeks.

I also have concerns about the cost of living persisting among many Chelmsford households, which may continue to impact sentiment and activity in the property market.

Additionally, the gradual impact of higher interest rates on those existing homeowners should not be underestimated. There are millions of homeowners whose existing sub 1% to 1.5% interest fixed mortgages are set to end in the coming three years.

Some of those Chelmsford homeowners would rather sell up and trade down market to reduce their mortgage outgoings than cut their household budgets regarding entertainment, holidays, etc.

However, as I have explained before in my Chelmsford Property Blog, my message to those homeowners is to speak with a qualified mortgage arranger. You will be amazed how extending the term of your mortgage will reduce your monthly payments, enabling you to stay in your existing Chelmsford home. Of course, you must weigh the pros and cons by talking to a qualified mortgage arranger.

Yet, if lots of Chelmsford homes get put on the market in the coming year or so (i.e., what happened in 2008), then we will have too much supply and probably not enough demand – meaning Chelmsford house prices will drop again.

The consistent rise in Chelmsford house prices over the past few years can be primarily attributed to a shortage of supply of properties to buy. The opposite will be the case if we get an excess supply of many homes on the market.

So that is what could go wrong in the Chelmsford property market; what about the potential good news?

Contrary to expectations back in late 2022, I stated a few weeks ago, Chelmsford first-time buyers in 2023 have been more active in the housing market despite prevailing uncertainty.

I attribute this trend to the rising rental costs, which have made homeownership in Chelmsford comparatively more cost-effective.

This, in turn, has attracted new Chelmsford landlords into the market to invest. I am aware some highly geared (i.e., they have high percentage mortgages on their buy-to-let properties) Chelmsford landlords have been battered with the section 24 taxation changes from a few years ago.

Yet, there are lots of new landlords coming into the buy-to-let market. They had their fingers burned on crypto and the stock market and are now looking for another investment vehicle for their savings.

The simple fact is the UK doesn’t build enough homes to satisfy the demand, meaning in the medium to long term, rents and house prices go up.

Buy-to-let is an excellent hedge against inflation (do ask me for my article from late last year about that).

The British housing market, which experienced a surge during the pandemic due to the demand for more space, has yet to experience the anticipated decline that some commentators predicted last year. The resilience of the UK economy, the strength of the labour market and the expected decrease in inflation throughout the remainder of the year are all factors that only add strength to the Chelmsford property market.

Tell me your thoughts on the matter – I would love to know them.

Lets get started! Our valuations are based on our extensive knowledge of the whole of the market.

Get a valuation

Property Market

23 Jul 2026

As an agent in the Chelmsford property market, I believ…

Property Market

Property Market

Property Market

Property Market