Blog

Blog

02 Jul 2025

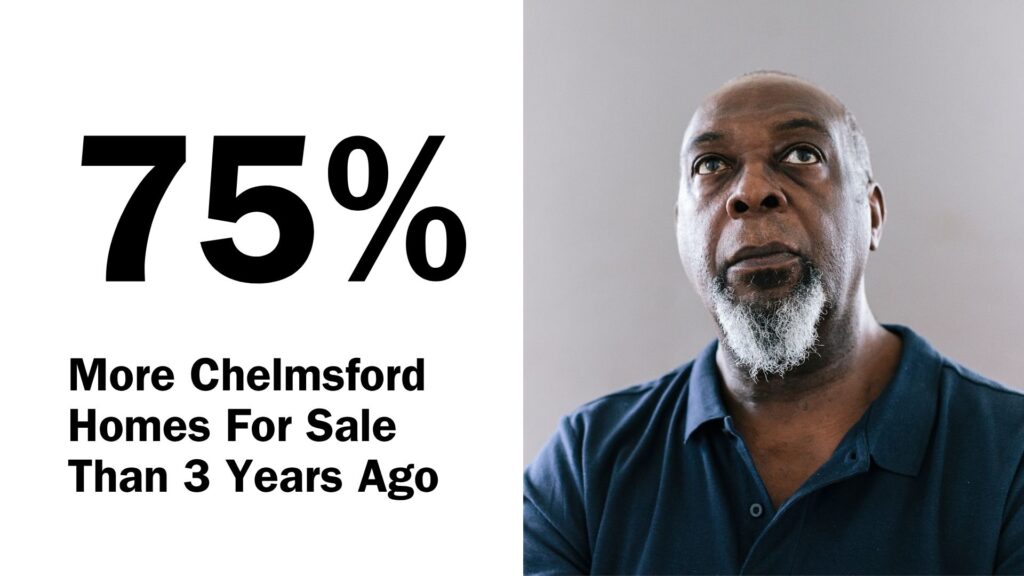

75% More Chelmsford Homes For Sale Than 3 Years Ago

At first glance, that number stands out. More homes. Mo…

Property Market

As we go into the second quarter of 2023, there is significant uncertainty in the UK economy, leading to uncertainty in the property market.

The number one issue is the fight against inflation and the cost-of-living crisis. The Bank of England is working hard to decrease inflation, and hopefully, in summer, we should see British inflation coming down. From that, we should expect interest rates to come down later in the year (and that is what the money markets believe with the 5-year swap rates).

This has driven mortgage pricing to the same levels seen the week before Liz Truss’ budget in September 2022. This will make homes more affordable because the mortgage payments would be lower.

Then there is the issue of house prices. Will they crash?

Later in the article, I will explain why 2023 differs entirely from 2008 (the last property market crash).

Yet it cannot be denied that the house prices achieved for Chelmsford homes today are lower than that completed in 2022. So why have house prices risen in the last few months in Chelmsford?

The devil is always in the detail. When the Land Registry reports on house prices from a particular month, it is actually from sales agreed six to nine months ago (because it takes on average four to five months from sale agreed to legal completion, then the solicitors have another two/three months to send the house paid data to the Land Registry).

That means the above increase in Chelmsford house prices is really from the sales agreed upon in the late summer of 2022.

Looking at what properties have been selling for this autumn and winter in Chelmsford, there are some minor reductions in the pipeline that will show later in the summer (because of the time lag of the Land Registry). Yet, as I discussed a few weeks ago when I was looking at £/sq. ft on sales agreed in February (not completed sales like the Land Registry), it is minor stuff.

Life events often drive someone to buy (or sell) a home. Every potential home buyer should ask themselves these two questions if they are considering a purchase.

If you answer yes to both questions, then buying now makes sense. But if the answer is no to either of these two questions, consider waiting until both answers are yes.

Being in the Chelmsford property market for as long as I have, the one thing I have learned, both personally and dealing with many people moving home in Chelmsford over the years, is this.

Note I say home and not a house. A house is a physical structure, whilst a home is a feeling. Don’t lose sight of the real reason for your endeavour – to build a home for yourself and those you care about.

Of course, Chelmsford house prices may fluctuate up or down in a 12 to 24-month period, but if you plan to have a minimum of at least five years in your new home, there are clear benefits to buying and owning a Chelmsford home.

Over time, home ownership always wins over renting.

I appreciate over the past few years many people have found it nigh on impossible to buy a home. In 2021/2, queues were outside open houses, multiple offers to one place, rocketing house prices, and limited homes for sale.

Yet, that has now changed. There is an increasing number of Chelmsford properties on the market.

Also, house prices achieved today are slightly lower than last year. That was to be expected as the ‘inflated’ Chelmsford house prices achieved in 2022 (because of the queues outside open houses, multiple offers to one place, rocketing house prices, and limited homes for sale etc.) aren’t being achieved today.

That means many Chelmsford people who couldn’t buy a home over the past couple of years are finding the market much more accommodating now.

What is the property market outlook for the rest of this year and the future?

Some people are trying to compare the current 2023 UK property market with the 2008 property market, yet there are significant differences between the two years.

Difference #1 is there is a massive amount of equity in homes today compared to 2008 (£189,500 today vs £135,900 in 2007).

Difference #2 was the stock levels of properties for sale.

The number of properties for sale in Chelmsford jumped from 950 in early 2007 to 1,826 in late 2007.

Even though there has been an increase in properties for sale in Chelmsford over the last six months (as mentioned in the article earlier), it has yet to be on the scale of the jump in 2007. This oversupply of the property market was a significant cause of house prices dropping in Chelmsford in 2008.

Difference #3 is there is a lot less unemployment in the economy today than in 2008 (3.2% today vs 5.6% in 2008).

Difference #4 is that most people (87%+) are on fixed-rate mortgages compared to 56% in 2008, so the increase in interest rates is not so much an issue compared to the run-up to the Credit Crunch in 2008.

There are other differences, but I want to avoid this turning into War and Peace!

Next, you must remember that in Chelmsford it isn’t just ‘one property market’.

There are ‘micro’ property markets within the whole Chelmsford property market.

There is still an undersupply of certain types of Chelmsford properties, meaning in those ‘micro’ property markets, supply can only partially satisfy the number of buyers wanting to buy a home, meaning house prices in those sections are holding up.

Yet on the other side of the coin, there is an oversupply of some other Chelmsford properties. Some of the increase in the overall number of properties on the market comes from overpriced Chelmsford homes in the ‘oversupplied’ micro property market.

If you want to know which ‘micro’ property market you are potentially selling in and potentially buying in (i.e., whether they are in an under or over-supplied ‘micro’ Chelmsford property market, drop me a line or send me a DM.

These are my thoughts, do let me know yours in the comments.

Lets get started! Our valuations are based on our extensive knowledge of the whole of the market.

Get a valuation Property Market

Property Market

Property Market

Property Market