Blog

Blog

02 Jul 2025

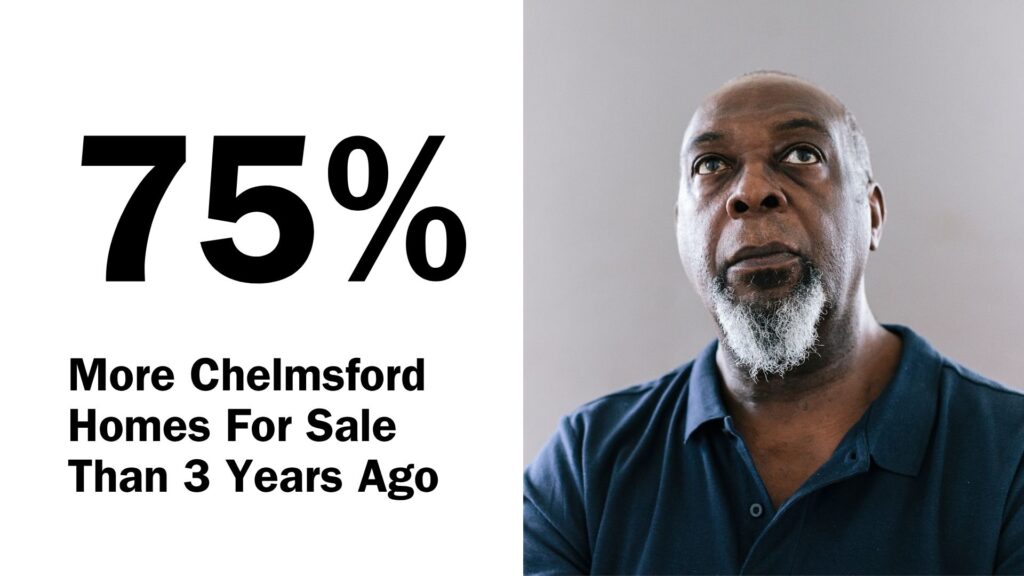

75% More Chelmsford Homes For Sale Than 3 Years Ago

At first glance, that number stands out. More homes. Mo…

Property Market

Embarking on the journey of homeownership is often seen as a rite of passage, but in Chelmsford, like many other places, young buyers may find it challenging without some assistance.

Enter the Bank of Mum & Dad, a pivotal driver in Chelmsford property market.

The term ‘Bank of Mum and Dad’ encapsulates the essence of parents contributing financially to their offspring’s pursuit of property ownership.

This concept has seen a surge in Chelmsford and beyond, as the “Bank of Mum and Dad” (BoMaD) continues to play a significant role in assisting younger (and sometimes middle aged) individuals, particularly in the property market.

In 2023, the average BoMaD gift or loan exceeded £25,000, with over half of under-35s who recently purchased a home receiving financial help from their families. The total value of BoMaD gifts amounted to £8.1 billion in 2022, facilitating 318,400 house purchases according to Legal & General.

Yet, not every parent in Chelmsford can afford to generously gift a deposit. Here, we explore varied avenues parents can explore to extend a helping hand in their child’s homeownership quest in Chelmsford.

Chelmsford property landscape is rich and diverse, making it an ideal locale for first-time buyers.

For Chelmsford homeowners pondering how to assist their children in this journey, rest assured that guidance is just a call away. Feel free to reach out to us with any queries you might have.

Lets get started! Our valuations are based on our extensive knowledge of the whole of the market.

Get a valuation Property Market

Property Market

Property Market

Property Market