Blog

Blog

02 Jul 2025

Sprucing Up Your Garden This Spring: Tips for Homeowners

As the sun begins to shine brightly in May and the gent…

Blog

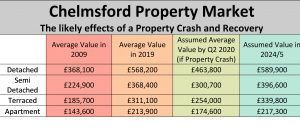

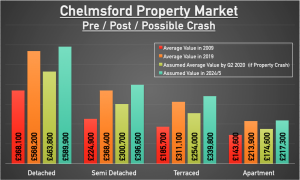

A handful of Chelmsford landlords and homeowners have been asking me what would happen if we had another property crash like we did in 2008/9?

On the run up to the Parliamentary vote on Brexit scheduled for March, a number of people asked what a no-deal Brexit would do to the property market and if there would be a crash as a result. I have discussed in a previous article on the chances of that (slim but always a possibility) … but assuming it happens, it is my opinion the outcome of a no-deal Brexit would be no worse than the country’s 2008/9 credit crunch property crash, the late 1988 property crash, the 1974 property crash, 1951 property crash … I could go on. The British economy would bounce back from the shock of a no-deal Brexit with lower property values and a continued low interest rate environment (together with an additional round of Quantitative Easing) and that would mean we would see a similar bounce back as savvy buyers saw it as a fantastic buying opportunity.

So, let me explain the reasons I believe this…

Initially, let’s see what would happen if we did have a crash, how quickly it would bounce back and then finally discuss how the chances of a crash are actually quite minimal.

Therefore, to start, I have initially split down the types of property in Chelmsford (Det/Semi etc) and in the red column put the average value of that Chelmsford property type in 2009. Next in the orange column what those average values are today in 2019.

Now, assuming we had a property crash like we did in 2008, when average property values dropped nationally by 18.37%, I applied a similar drop to the current 2019 Chelmsford figures (i.e. the green column) to see what would happen to property values by the middle 2020 (because the last crash only took 13/14 months).

…and finally, what would subsequently happen to those same property prices if we had a repeat of the 2009 to 2014 property market bounce back.

Of course, these are all assumptions and we can’t factor in such things as China going pop on all its debt … yet either way, the chance of such a crash coming from internal UK factors are much slimmer than in another of the four property crashes we have experienced in the last 80 years. Why, you might ask?

The seven reasons I believe are these …

So as the circumstances are much different to the last two crashes, the chances of a crash are much slimmer. Yet if we do have a crash, for the very same 7 reasons above why the chances of a crash are unlikely, those 7 reasons would definitely contribute to making the ensuing recession neither too long nor substantial in scale.

One final thought for the homeowners of Chelmsford. Most people when they move home, move up market, meaning in a decreasing market you will actually be the winner, as a 10% drop on yours would be much smaller in £notes than a 10% drop on a bigger property … think about it.

One final thought for the new and existing buy to let landlords of Chelmsford. Well, the questions I seem to be asked on an almost daily basis by landlords are: –

Many other Chelmsford landlords, who are with us and many who are with other Chelmsford letting agents, all like to pop in for a coffee, pick up the phone or email us to discuss the Chelmsford property market, how Chelmsford compares with its closest rivals (Braintree, Bishops Stortford and Maldon), and hopefully answer the three questions above. I don’t bite, I don’t do hard sell, I will just give you my honest and straight-talking opinion. I look forward to hearing from you.

Lets get started! Our valuations are based on our extensive knowledge of the whole of the market.

Get a valuation Blog

Blog

Blog

Blog